Green Bluff Real Estate Newsletter

The Green Bluff Real Estate newsletter for Winter/Spring 2025 summarizes the real estate market activity that happened for 2024 with all of its ups and downs.

Interested in keeping up with Green Bluff farming and events? Check out the Green Bluff Growers here: Green Bluff Growers

Election Year Drama

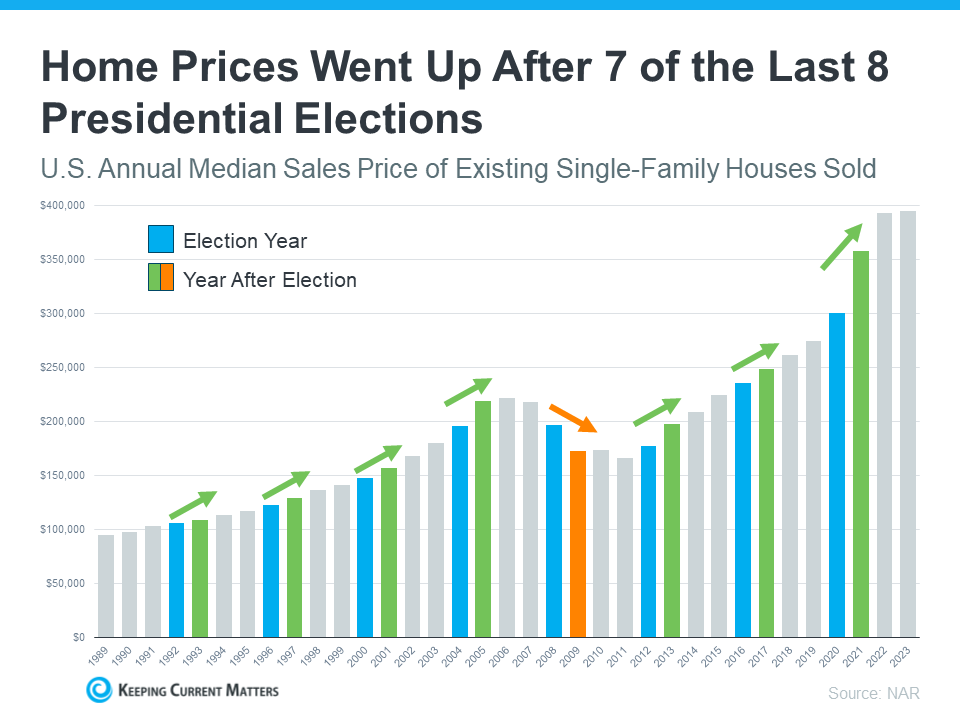

Election years usually bring drama, but let’s be real: they can shake up the housing market. The 2024 presidential election is no exception. If you’re wondering how it might impact your real estate plans in 2025, here’s the scoop—without all the political drama.

Historically, housing markets can experience a shift in buyer and seller behavior during election years. Some buyers and sellers tend to hang back, uncertain about the future. This could mean less competition, which might be good if you’re buying. On the flip side, the uncertainty can make sellers hesitate, making inventory more stable. More stability means a more predictable market—whether you’re buying, selling, or just enjoying the view.

Housing markets often thrive after election results are in—regardless of who wins. Once the uncertainty fades, consumer confidence tends to rise. In Green Bluff, we could see that confidence manifest in more buyers jumping back into the market, especially with the charming rural vibe and proximity to Spokane. Despite the election jitters, history shows that the market typically rebounds after the results are in, both with increasing prices and more sales activity. So, while the election might bring its share of political noise, the housing market is more likely to hum along in a steady rhythm.

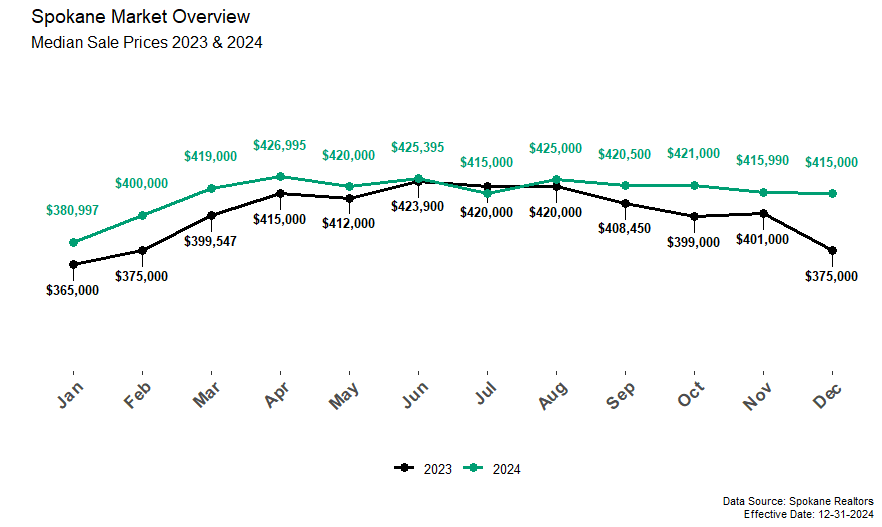

Summary of Spokane Sale Prices

Is it Safe to Assume?

What’s a Loan Assumption?

Real Estate Loan Assumptions: Saving Big Bucks in a High-Interest World

Let’s face it: in today’s real estate market, interest rates are as high as your stress level on a Monday. But what if there was a way to dodge the bullet of sky-high interest rates and save thousands of dollars in the process? Enter the magic of loan assumptions.

What’s a Loan Assumption, Anyway?

In simple terms, a loan assumption happens when a buyer takes over the seller’s existing home loan. For example, let’s say a seller has a 3% mortgage, but today’s rates are a whopping 7%. With an assumption, the buyer could “assume” the seller’s low-interest loan instead of signing up for today’s cringe-worthy rates. You could walk away with a loan payment way lower than today’s norms, all thanks to that low rate.

How Loan Assumptions Could Help Buyers and Sellers:

Buyers: Here’s Your Chance to Save a Boatload of Cash

In a world of skyrocketing rates, loan assumptions could be your meal ticket. Imagine snagging a loan with an interest rate that’s practically a relic of the past. It’s like finding a vintage car that still runs like a dream—and at a fraction of the cost of a brand-new one. Assuming a loan can save you thousands in interest over the life of the loan, and that’s a win any day of the week. Plus, the lower your interest rate, the more you can put toward your principal—meaning your home could be paid off faster than a politician changes his mind!

Sellers: A Clever Way to Stand Out

Sellers, you may be wondering, “How does this benefit me?” If you’re sitting on a low-interest mortgage, offering a loan assumption could make your listing more attractive to buyers who are tired of the interest rate roller coaster. It’s like offering them a first-class ticket while everyone else is stuck in coach. But here’s the thing: not all loans are assumable. You’ll need to check with your lender to see if your mortgage allows it. If it does, you could be looking at some serious demand from buyers, increasing the odds that your property could sell for top dollar.

Bottom Line:

In a market with high interest rates, loan assumptions could be gold for both buyers and sellers. Buyers can lock in a great deal by assuming a low-rate mortgage, and sellers can make their home more appealing by offering the chance to do so. It’s a win-win situation—no magic required! So, before assuming there’s no lower rates to be found, take a second look at loan assumptions. You might just find that the best deals are hiding in plain sight.

Green Bluff Real Estate 2024 Market Summaries

Sale Prices and Odds of Selling

Green Bluff average and median prices are down ranging from about -3.0% to -9.0%. Many properties have higher price tags, and, as a result, they are harder for buyers to afford. With fewer people who can afford these properties, the buyer market is much smaller. In some cases, many of these properties don’t sell. In fact, for 2024, the odds of selling was 52%, which means 48% of all properties listed for sale didn’t sell!

Supply and Demand – Loan Rates

With low demand, prices often come down, which is exactly what happened in 2024. High loan rates contributed to low demand and reduced prices. Rates averaged about 6.75% in 2024, peaking at 7.22%, but they’re still lower than the historical average of 7.7%.

Days on Market

Properties priced below $1,000,000 were getting an offer in an average of 31 days after being listed for sale; properties priced $1,000,000 and higher were taking 166 days on average to get an offer. Just expect it to take longer to sell a higher priced property as there aren’t many buyers with the resources to make that kind of purchase. With the election chaos over and consumer confidence on the rise, based on historical trends, prices will likely increase in 2025.

Election Years and Home Prices

More details about the impact of elections on the housing market from Keeping Current Matters can be found here.

Contact Cody Kerr:

Leave a Reply